Tokenomics Fundamentals Series: W5H framework for token design, Part IV - Token supply and demand dynamics

W5H tokenomics framework Part IV: following "Why, When, What, Where, Who and How" for token design, we discuss token supply-demand dynamics

Table of Contents

- Regulating token supply and demand

- Token supply regulation

- Regulating token demand

- Token supply and demand analysis

- What value creation drives the token demand and is it sustainable?

- How will the token supply change, and can the demand match it?

- Case study 1: OlympusDAO and OHM

- Case study 2: Axie Infinity

- Conclusion

This article is part IV of the following six-part series:

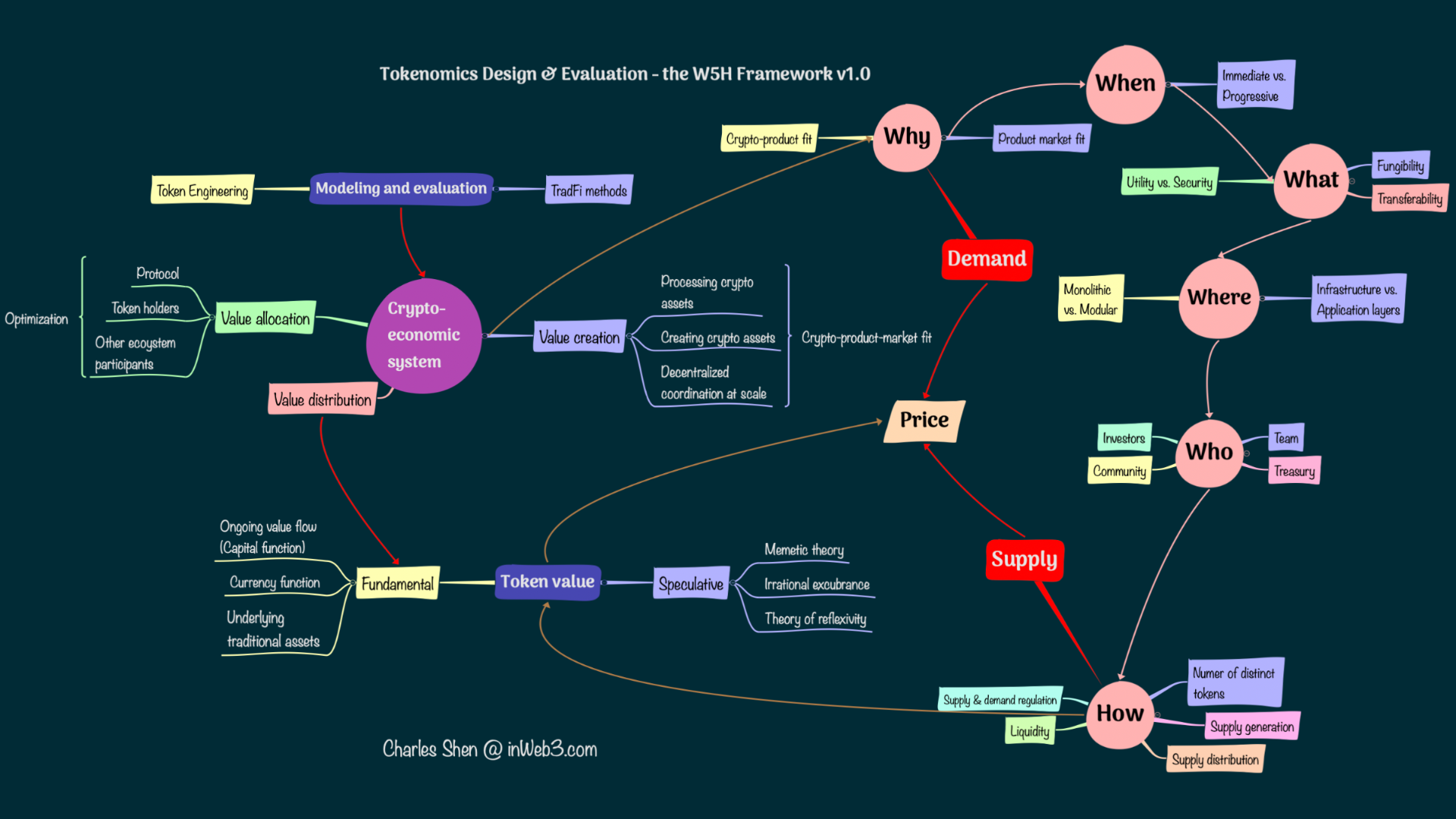

In the prior parts of the series, we discussed the “Why, When, What, Where, Who, and How” of token design.

W5H framework for token design (W5H) by Charles Shen @ inWeb3.com

W5H framework for token design (W5H) by Charles Shen @ inWeb3.com

While many of our discussions are in the context of the initial token launch, answers to these questions directly impact the ongoing supply and demand in the ecosystem, which is crucial for the long-term sustainability of the token project. The dynamic equilibrium of supply and demand at the overall business level and the token level determine the prices of goods and services as well as the tokens. They are the remaining critical components that close our W5H loop, and are the focus of this article.

W5H framework for token design (Supply & Demand) by Charles Shen @ inWeb3.com

W5H framework for token design (Supply & Demand) by Charles Shen @ inWeb3.com

As usual, we approach the supply-demand dynamics at both the business level and the token level. At the business level, the supply and demand of specific goods and services are actually part of the crypto-product-market fit problem discussed in “Why token”. Therefore, let us elaborate more on the token-level supply and demand mechanisms here.

Regulating token supply and demand

Token supply regulation

Token supply may be regulated through a project’s governance. Recall from our “How” token part that token supply generation can be pre-scheduled or on-demand. If the supply is pre-scheduled, some projects’ governance chooses to modify the original token emission pattern when the situation changes, to adjust the future token supply. If the token minting is demand-driven, there are also things the project’s governance might be able to do to adjust the supply. For example, if a stablecoin is minted based on collaterals, then setting a lower required collateralization ratio leads to more supply of the stablecoin. However, such change has consequences. Lower collateralization ratios bring increased risk to the project’s overall financial status.

While supply regulation could mean both increasing and reducing supply, the more prevalent issue projects encounter is the over-supply of tokens that cannot be sustained by their demand. Let us focus on mechanisms that reduce token supply in more detail.

Temporary supply reduction - locking and vesting

Locking tokens temporarily removes them from the circulating supply and reduces the token’s selling pressure during the lock period. A vesting schedule releases the tokens gradually over time, alleviating abrupt supply shocks. The project could set up incentives to encourage voluntary locking by the token holders. The more real value these incentives bring to the users; the more effective the mechanism could be. For example, the well-known veCRV model of Curve Finance locks the CRV token for up to four years in exchange for governance rights and for sharing ongoing protocol fees. Derivative protocols built on the veCRV mechanism, such as Convex, even turn the locking of CRV from temporary to permanent, further tightening the token selling pressure.

Note that the more tokens locked does not necessarily mean the more valuable the token becomes. For example, if a token serves as a medium of exchange for goods, and nobody can get the token because all tokens are locked, then the exchange for goods cannot happen, and the overall crypto economy would not even exist.

Permanent supply reduction - burning tokens

Burning existing tokens can permanently remove them from the circulating supply. It artificially introduces a deflationary force to counter the token’s inflationary pressure and potentially improve token value. Common token-burning mechanisms try to tie the burning process with the token demand. One approach is to burn tokens when users spend them on the protocol’s services. ETH’s EIP1559 implementation burns part of transaction fees. BNB has a similar real-time partial transaction fee burning. The Graph protocol that provides blockchain data query services also burns a portion of its fees received both from the querying users and the node service providers.

When the burning mechanism is meant to counter token inflation, designing the right parameters to strike a real-time token supply-demand balance could be very challenging because of unpredictable factors in the economic system. One approach people use is to periodically assess the demand condition to decide how much supply should be reduced, then buy back and burn them. The BNB token’s quarterly auto-burn, e.g., determines the burning amount by the BNB token price and the token supply-demand dynamics, which means that more tokens will be burned if the price of BNB declines.

Smoothing and reduction of future token supply

Supply smoothing and reduction may also be applied to tokens not yet released.

- Tokens scheduled for future release typically adopt a relatively smooth emission pattern rather than a step function-based inflation leap. Convex protocol’s pre-scheduled CVX token emission is an example of a smooth minting curve with a reduced inflation rate. For tokens that are designated for specific participants, especially those at low or zero cost for investment or rewards, a norm is to enforce a mandatory lockup and vesting period. For instance, teams and VCs typically receive their allocated tokens after a locked period of less than one year to a few years. These tokens are usually vested gradually in 1 to 3 years. Similar locking and vesting can be applied to token rewards earned by yield farming, e.g., as in the DeFi Kingdom game.

- We have also seen projects adjusting their future release schedule to explicitly cut emissions. E.g., the Sushi token started with an infinite inflation schedule. Later its governance deemed it too aggressive and approved a 250M hard cap for the token. The Cosmos 2.0 whitepaper released in September 2022 proposes changing the ATOM token’s long-term emission schedule from an exponential expansion to a more contained linear schedule. But it also requires a significant short-term increase of token emission and was rejected along with other amendments.

Regulating token demand

Handling supply and demand dynamics does not have to be limited to the supply side. It is possible to stimulate or suppress demand in response to changing supplies caused by external factors. The DAI savings rate mechanism of MakerDAO offers a good example. In a basic scenario of MakerDAO’s DAI stablecoin, people deposit their ETH tokens as collateral to mint DAI, increasing DAI supply. In a crypto bull market, people are more likely to take on ETH leverage to mint DAI, resulting in more DAI supply and relatively weaker DAI demand. At such times, the protocol may reward people for holding DAI by raising the DAI savings rate, thus increasing the DAI demand to bring the supply-demand relationship towards a more balanced position. In a bear market where people prefer more stability of holding DAI, the demand is stronger than the supply of DAI because people tend not to leverage ETH to mint DAI. In response, the protocol can reduce the DAI savings rate, practically discourages people from holding DAI, and suppresses its demand.

Token supply and demand analysis

We can ask three common questions when examining token supply-demand dynamics and the resulting token price. Two of them will be discussed in this section, and the third one on token value capture will be covered in the next part of this series. We also select two symbolic projects from the recent crypto market cycle to illustrate the application of the presented questions.

What value creation drives the token demand and is it sustainable?

We temporality ignore the supply side when addressing this question. The system should have sound fundamentals that support a consistent and increasing demand for the token. We can review our answer to the “Why token” question, diving deeper into the token project’s business model and its value creation process. Are there meaningful services and products that produce revenue? Where does the revenue actually come from? Is the revenue sustainable? How do the revenues compare with the costs?

- If a system is not financially sustainable yet but provides meaningful services, it could still be successful. Just like companies in the tech world that are losing money during the growth period. These projects could receive external funding (primarily from VCs) that helps them through those early periods. Of course, there is no guarantee that such projects will indeed prevail; many of them inevitably fail.

- If a system seems profitable but relies primarily on a constant influx of new user funds to sustain its business model, that should raise a flag for potential “ponzinomics”.

How will the token supply change, and can the demand match it?

If the crypto project passes the fundamental demand drive test under a given token supply, we still need to check whether the changing token demand and supply can achieve a healthy balance.

If supply decreases, it should help push the price higher in the short-term given similar demand. But if supply decreases too much, it might stifle the demand and harm the overall economy. Therefore, many token economies are designed to have moderate supply inflation. This inflationary supply can either follow a pre-determined schedule or be released “on demand.” Let us look at what could happen to the new token supply:

- People may sell them on the market and cash out; this is the least wanted case since it indicates higher supply and lower demand, which pushes the price down.

- People may hodl the token for the long term. This behavior is desired as it signals higher demand and temporarily takes the new supply out of circulation, reducing selling pressure.

- People may spend the new tokens on a service that burns them (when applicable). This outcome also represents demand for the token and is highly desirable since it essentially negates the extra supply and minimizes the delusion of the new supply.

- Other user behaviors could lead to various degrees of demand impact in between the ones listed above.

If aggregate impact from user demand consistently falls short of matching up with the supply, the economy could fall into a hyperinflation mode and lead to a token price crash.

Case study 1: OlympusDAO and OHM

OlympusDAO is a representative project for DeFi 2.0. It aspires to “create a decentralized, censorship-resistant reserve currency for the emerging Web3 ecosystem”. Its OHM token intends to preserve purchasing power, maintain deep liquidity, and serve as a unit of account and a store of value reserve. But unlike crypto stablecoin projects, the OHM token is not pegged to Dollar. Instead, it is backed by assets such as the decentralized stablecoin DAI. The change from “pegged” to “backed” is significant. It means OHM has a free-floating value, but its intrinsic value is its underlying backed asset.

What is the primary value that draws users to the OHM token?

When OHM was launched in early 2021, its immediate demand driver was not its status as currency because it was yet to be adopted. Instead, it offered a passive earning APY as high as six figures for staking OHM. Even in mid-2022, the APY was still at the middle three figures level. The incredible API, along with its (3,3) meme, were the main factors people buy and stake OHM at the time.

Where does the yield of OHM come from, and is it sustainable?

A deeper look into the protocol reveals that the early APY comes mainly from the protocol selling OHM to buyers willing to pay far more than the one DAI-backed intrinsic value. But why would people be willing to pay a much higher price, which at the top reached $1415 in April 2021, knowing the intrinsic value is backed by roughly $1? Some users may think the project’s future growth, including the massive treasury assets the protocol controls through the bonding mechanism, is worth the premium. Others may FOMO into it because of the (3,3) meme. If everyone does cooperate and buys only, the price keeps going up. If the price keeps increasing, getting in early gives you a better price and a higher share of the protocols’ value accrual. The only problem is, for the price to keep going up, there need to be unlimited new buyers entering the system. When the new buyer inflow stops, the system turns into Ponzinomics rather than Tokenomics. Jordi Alexander from Selini capital has more insights on this topic.

Summary:

Overall the Olympus protocol has some impressive design, with an ambitious goal and a once wildly popular meme. Unfortunately, its model lacks a sound fundamental and is not sustainable. In hindsight, it should not be too surprising to see OHM price fall by over 99% from its ATH.

Nevertheless, the Olympus project has also produced some impactful innovations, especially the concept of protocol-owned liquidity, which is considered a key characteristic of DeFi 2.0. The protocol still has nearly 250M of Treasury Assets in early 2023.

Case study 2: Axie Infinity

Axie Infinity is an NFT-based blockchain game. Players battle, collect, and trade NFT digital pets called Axies. It is the symbol of play-to-earn games.

What is the primary value that draws users to the Axie Infinity game and its tokens?

Many players were attracted to Axie Infinity for the prospect of earning income. A May 2021 Twitter poll conducted by the game developer indicates that 48% of the nearly 1000 respondents are in for the “Economy” vs. only 15% for the gameplay. That means a large proportion of the participants are looking for a job, not for a game.

Where do the earnings from the game come from, and is it sustainable?

If people are in the game to earn, where does that money come from? Unfortunately, the early Axie Infinity economy does not generate self-sustaining revenues. It requires players to pay an upfront amount to buy the gaming NFTs to start playing. At its peak, the price tag for the entry NFTs ranges from hundreds to over $1K. The continuous influx of new users paying the cost to join the game has been what supported a token price level that allows existing players to cash out and earn a meaningful income. However, it’s impossible to expect an unlimited number of new users to join the system at an increasingly higher price tag. When new user growth slows down, the token price drops, and existing “worker” players cannot earn enough to make a living. They may leave the game, causing a downward spiral. In short, the demand side fundamental of the game does not pass the sustainability test.

How will the token supply change?

The Axie Infinity game has been acclaimed for providing low-income communities with a play-to-earn model to make a living. That is indeed a worthy cause. A guild-based scholarship mechanism is also created to help onboard more users who cannot afford the game entry NFTs. The idea is to let them borrow the necessary NFTs to start playing. They can later pay back their loan and keep the rest of the earnings. This mechanism worked and effectively brought in a large number of users to the game. At one time, an estimated 60%-65% of the people who own Axies are scholars.

However, so many new users entering the system also means accelerated token supply, e.g., people winning more of its SLP tokens in the game. This situation adds to the existing inflation pressure caused by bots that further push the minting of more tokens in the game.

Can token demand match the supply change?

On the demand side, users can sell the earned SLPs and cash out. Then these SLPs are added back into circulation as inflation. The users can also spend those SLPs to breed Axies. That will burn and deflate SLP tokens. Therefore, the outcome will be determined by the comparable speed of SLP inflation vs. deflation. An analysis of SLP minted vs. burned by NAAVIK shows that after August 2021, the SLP minting speed has been faster than its burning speed, and the mint/burn ratio continued to accelerate. Apparently, the deflation power is not strong enough to offset the increasing supply. This phenomenon is probably not surprising if we recall that most of the scholars and low-income players treat the game as a job to win the SLP tokens and sell them for cash earning. They are mainly using the inflation route, not the deflation path.

Source: CoinGecko and NAAVIK

Source: CoinGecko and NAAVIK

If we look at the price of the SLP token and its market cap, August 2021 marked a period when the SLP token price started a quick descent from near $0.34 to a range between $0.05 and $0.10. This pattern suggests that the game suffered a hyperinflation problem.

Source: CoinGecko and NAAVIK

Source: CoinGecko and NAAVIK

Balancing a game economy has never been an easy task. Solving the in-game SLP hyperinflation issue requires the designers to reduce the token inflation source and/or increase the deflation sink. But these decisions often bring dilemmas. Reducing the number of SLP token rewards also changes the incentives for players and could affect their engagement. On the other hand, limiting the number of Axies could be a way to encourage breeding and thus leads to more SLP burned. But it may also result in higher Axies price that further increases the barrier for new players to join.

To their credit, the team publicly acknowledged these problems and has been working in various directions to improve them. They addressed the hyperinflation problem by making it more difficult to earn SLP tokens and imposed further control on the number of Axies. For the fundamental question of actual revenue generation, they listed several options on the Axie Economy & long term sustainability page. They also released a free-to-play version of the game as part of those efforts, potentially onboarding more people from the broader player community and earning revenue from in-game items.

Conclusion

This article follows our prior coverage of the “Why, When, What, Where, Who, and How” of token design, and explored the dynamic equilibrium of supply and demand that closes the W5H loop. Since supply and demand dynamics at the business level is part of the prior “Why token” discussion, we looked at various ways to regulate supply and demand at the token level in this article. Using two symbolic crypto projects as case studies, we also elaborated on two questions covering both the business and token levels, that help examine the supply and demand relationship of a given crypto project.

One remaining question we have not delved into is the connection between the two levels. Specifically, how the value created at the business level accrues to the token level. This is a key aspect of tokenomics design that impact the valuation and pricing of the tokens. It will be our topic in the following part of this series.

This article is part of the six-part W5H framework for token design series, as listed below:

Related Articles

Tokenomics Fundamentals Series: W5H framework for token design, Part VI - Token value assessment

W5H tokenomics framework Part VI: token value assessment through TradFi modeling and their caveats, and a brief introduction to Token Engineering.

Tokenomics Fundamentals Series: W5H framework for token design, Part V - Token value accrual

W5H tokenomics framework Part V: token value accrual through universal and selective economic value distribution in crypto-economic systems

Tokenomics Fundamentals Series: W5H framework for token design, Part III - How Token?

W5H tokenomics framework Part III: following the prior "Why, When, What, Where, and Who" for token design, we continue to explore "How token".