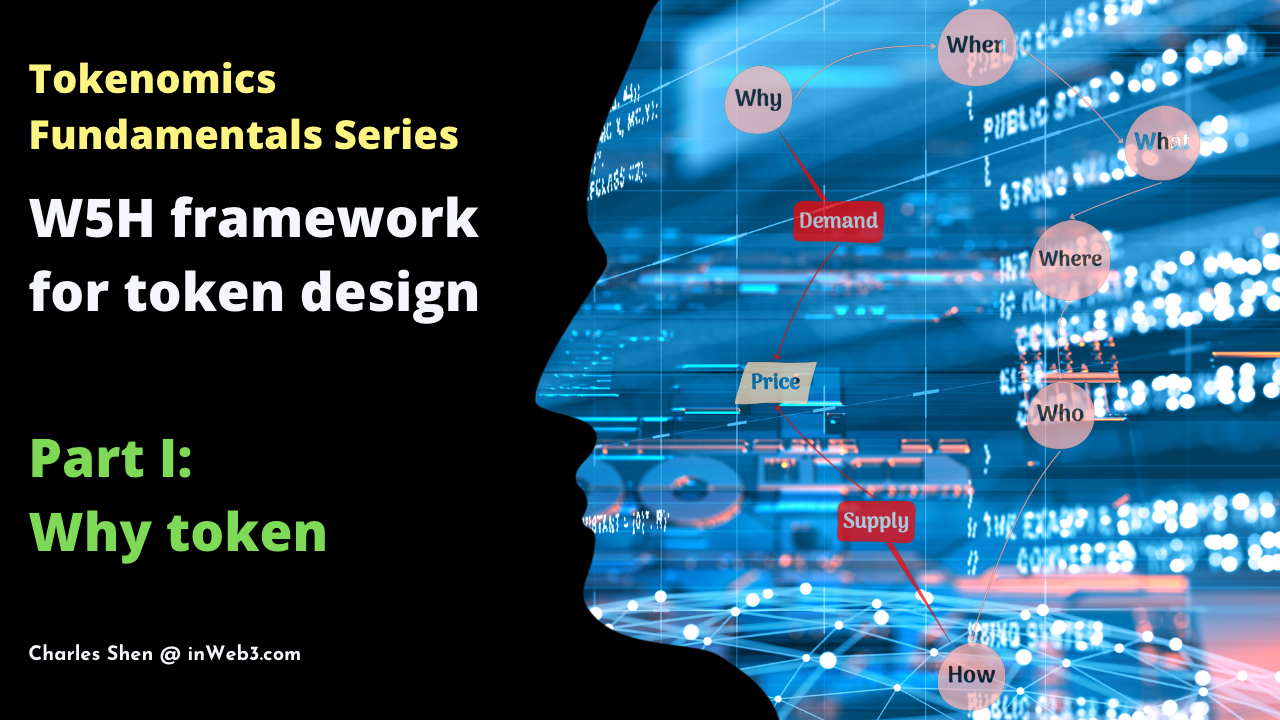

Tokenomics Fundamentals Series: W5H framework for token design, Part I - Why token?

W5H tokenomics framework - "Why, When, What, Where, Who and How" for token design. Part I, "Why token" - a crypto-product-market fit perspective.

Table of Contents

This article is part I of the following six-part series:

Tokens are atomic units of Web3. The success or failure of token design often determines the fate of crypto projects. A key term the industry used to judge the token design is its tokenomics, which is a portmanteau word from “token” and “economics”. Tokens with good tokenomics enable the crypto project to form a thriving micro-economy and provide a powerful flywheel that drives continuous economic value growth. In contrast, poor tokenomics witnesses its token value crashing and is detrimental to a crypto project’s sustainability. Tokenomics can be considered one of the three pillars in the blockchain-crypto infrastructure, along with distributed consensus and smart contracts.

Tokenomics is, however, is a challenging topic to grasp especially for people new to the space. The term is often used as a catch-all word that reflects mechanisms stemming from many disciplines, such as economics, engineering, psychology, and behavioral sciences.

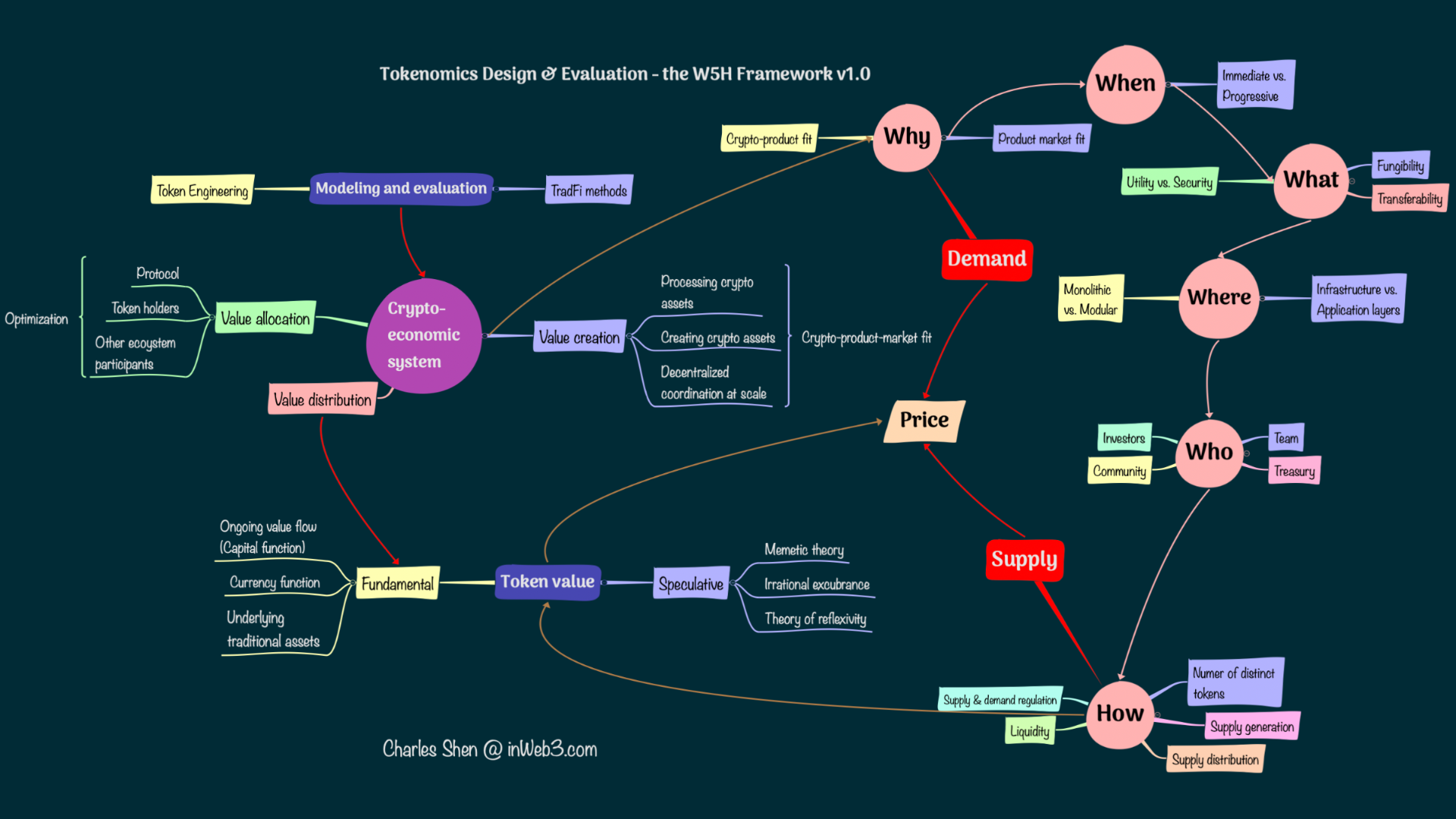

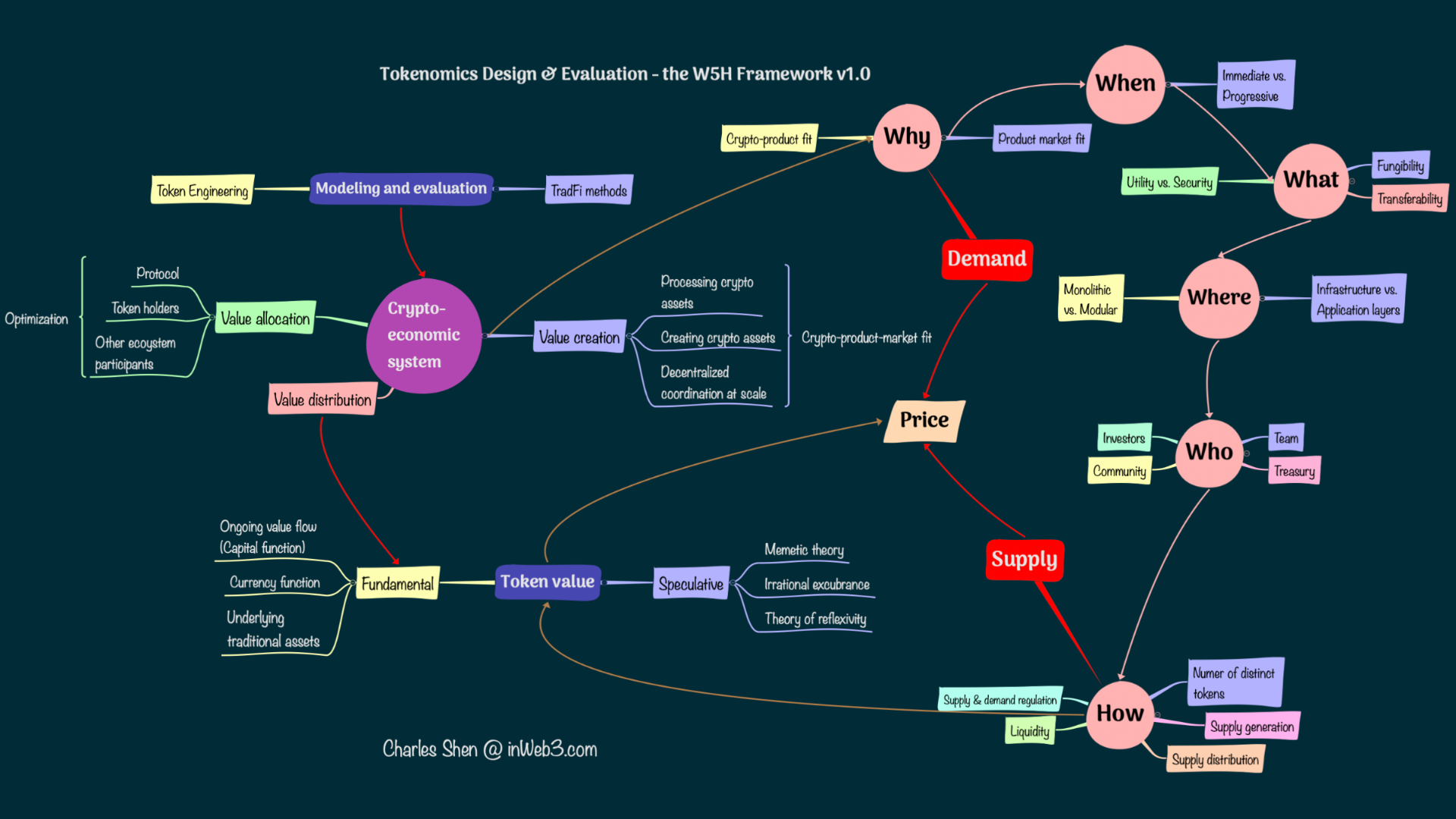

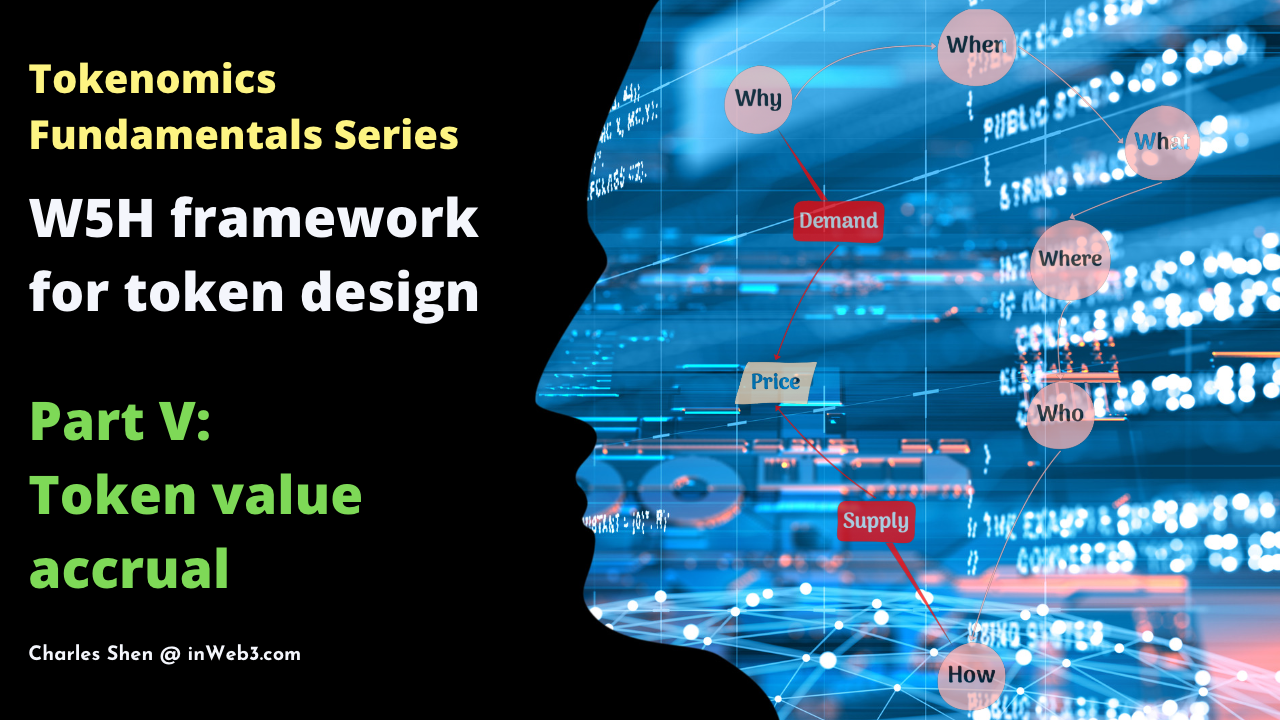

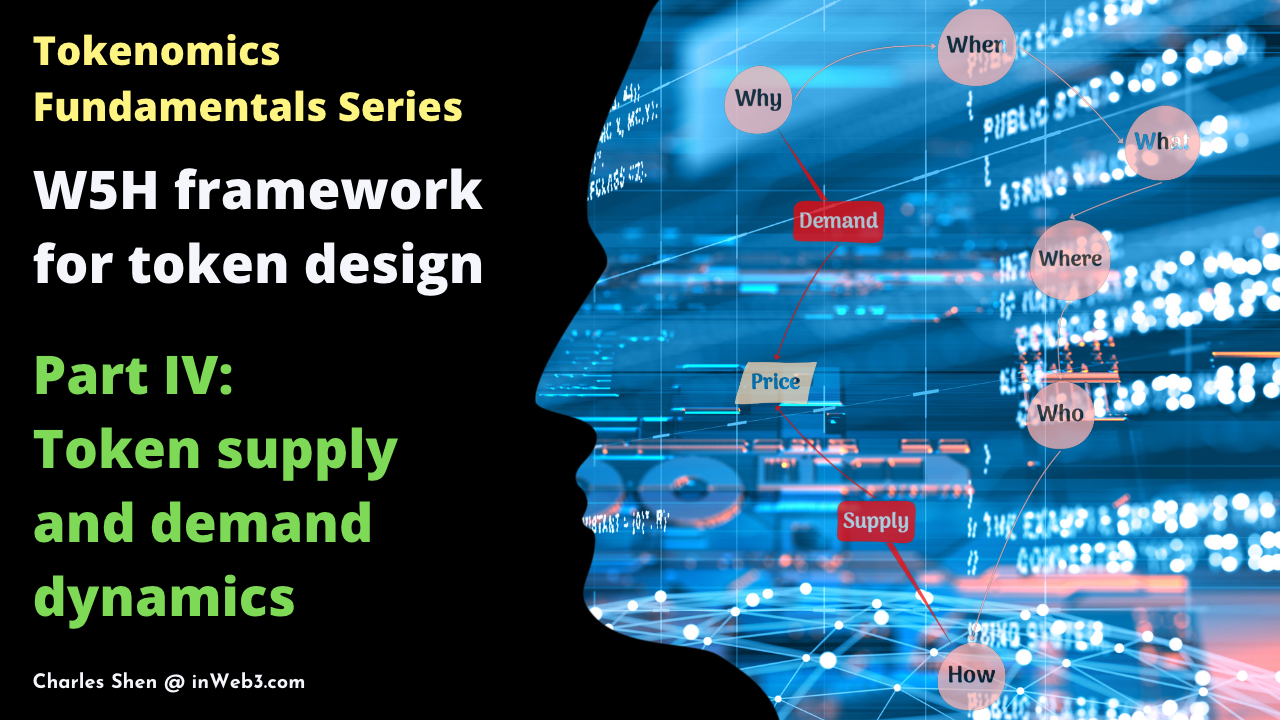

In this series, I introduce a beginner-friendly framework for token design summarized as Why, When, What, Where, Who, and How (W5H). The backbone of the W5H framework is illustrated below:

W5H framework for token design (Backbone) by Charles Shen @ inWeb3.com

W5H framework for token design (Backbone) by Charles Shen @ inWeb3.com

- “Why” examines the rationale for the token and sustainable value creation of the token’s underlying crypto-economy;

- “When” checks the best timing for launching a token;

- “What” investigates the type of tokens that is suitable for the use case;

- “Where” focus on the blockchain network stack where the token should reside;

- “Who” looks into the appropriate parties in the ecosystem that should own the token;

- “How” talks about topics such as determining the number of distinct tokens needed, the token supply generation, allocation, distribution, and liquidity provisioning.

The W5H loop is then closed by the supply-demand dynamics of the crypto economy. The equilibrium of supply and demand ultimately affects the price of goods and services in the economy and the token itself.

The W5H framework provides a way to understand tokenomics in the context of the broader token design. It places us in the driver’s seat of the token project, guiding us through the rationales behind the most important aspects of related token mechanisms. Therefore, it can help builders who are designing a new token, and also investors or users who are evaluating an existing token.

A crucial principle when applying this framework is to first look through the lens of the business associated with the token and then place token-specific considerations. This is because a token is an integrated part of the crypto economy, and it derives its value from there.

We will cover our presentation of the W5H framework in a series of six articles. At the end of this series, we should have covered the topics illustrated below:

This is the first article in the series where we will focus on “Why token”.

Terminology review

Before we actually start, let us review the meaning of several key terms we will be seeing frequently in this series: “Token”, “Crypto”, “Crypto-economics”, and “Tokenomics”. If you are already familiar with them, feel free to skip this section. If you are new and want to review more of the related terms, please refer to the terminology page and the articles in the introduction to Blockchain, Crypto, Metaverse, and Web3 series.

Token: in a general sense, a token represents something of economic or social value. It could be a coupon, a movie ticket, or a stock certificate. In the blockchain context, we are concerned about “cryptographic tokens”, which are digital tokens created and managed through blockchains powered by cryptographic mechanisms.

Crypto: people commonly associate the word “crypto” with cryptocurrency. Since cryptocurrency may be considered a subset of cryptographic tokens. “Crypto” may be used as a general term for cryptographic tokens, regardless of whether they have currency-like utilities.

Crypto economy and crypto-economics (aka cryptoecon): crypto projects typically involve various token transactions. These transactions form the basis of the economies surrounding those projects. We refer to these economies as crypto economies and the study of them as crypto-economics. Both endogenous and exogenous tokens could contribute to a crypto economy. In the author’s view, crypto-economics is more naturally applied at a project level rather than to an individual token.

Token economy and token economics (aka tokenomics): the token economy is a concept closely related to the crypto economy. While they are sometimes used interchangeably, there have subtle differences. The token economy and its associated tokenomics are typically specific to individual tokens. Great tokenomics requires great crypto-economics that creates sustainable value. But the reverse is not necessarily true, because the tokenomics needs to address whether and how the value created in the crypto economy is accrued to the specific token (which is a topic we have a deep dive into in Part V of this series.)

Why token

While the token design is critical to token-based projects. That does not mean all crypto projects must first create their own tokens to prosper. In fact, a prudent token designer should always start by asking: “Why would this project need a token in the first place?”

When we ask this question, we typically mean a token that is specifically created for the project, also known as the project’s native token. This is to be differentiated from any other exogenous tokens that the project may be processing. For example, the decentralized exchange Uniswap has a UNI token as the project’s native token, but the exchange serves the transactions of numerous other tokens, which are all non-native to the project.

One possible answer to the “Why token” question is that tokens may help raise capital for the project, with additional benefits that allow early community members to invest in the project and gain upside. In contrast, early-stage equity investment opportunities are usually limited to accredited investors. Nevertheless, the upside of an early token project is never certain, and there are also notable legal unclarities in that practice. Therefore, the fundraising aspect is one of the rationals, but should not be the only and core answer to the question.

My preferred way to address the “Why token” question is to treat it as a crypto-product-market fit problem, which we can examine in two steps: crypto-product fit and product-market fit.

Crypto-product fit: why integrate crypto into the business model?

Let us start with the crypto-product fit and take two complementary perspectives: one focusing on the role crypto plays in a product, the other looking at the economic sectors crypto may be integrated with.

Crypto’s role in crypto-product business models

Crypto and its underlying blockchain infrastructure are equipped with a few key technology pillars that enable their unique value proposition:

- Distributed consensus mechanisms form the basis for creating a distributed ledger that maintains transaction record immutability and transparency.

- Smart contracts capabilities offer programmability to realize arbitrary business logic incorporating various types of transactions.

- Tokenization allows the digital representation of values and enables them to flow through transactions across a global distributed ledger.

While every project may use crypto in different ways, the above characteristics make possible three most common types of crypto-product business models:

Type A: Processing external crypto assets (tokens that already exist), without the need to create their own token.

- Crypto exchange is an example that belongs to this type. Coinbase is a centralized crypto exchange and does not need its native token to function. Uniswap is a decentralized crypto exchange deployed as a smart contract on the Ethereum blockchain. It started without its token. Even though it later introduced a UNI token, the token is for governance and is not required by the core exchange service.

Type B: Creating new tokens through the tokenization of assets and enabling efficient transactions (e.g., transfer, exchange, verification, etc.) of these tokenized assets through a global distributed ledger. These assets could be of any type - financial assets, real assets, and intangible assets.

- For financial assets, USDC is an example that tokenizes the fiat US dollar and creates a stable cryptocurrency for spending in the crypto world and many non-crypto places.

- For real assets, companies are working on tokenizing real estate, agricultural commodities, and rare wines, which helps improve these industries’ efficiency.

- Examples of tokenized intangible assets include BAYC Non-Fungible Token (NFT), which bestows club access rights in a unique social circle, and POAP NFTs that certify people’s event attendance records as part of a reputation-building process.

Type C: Creating and leveraging tokens to enable decentralized autonomous coordination at scale. The tokens in this category typically have utility functions and/or governance rights. These tokens are often used as incentives to orchestrate the value flows toward the ecosystem’s collective objectives. There are several common product categories under this type: infrastructure, application, and human-oriented services.

- Bitcoin network is an example of an infrastructure product. It uses its BTC utility token to direct the value created by its network to a decentralized group of miners. This arrangement incentivizes the miners to contribute hash rates to maintain network security, which is critical for the Bitcoin system’s operation. Other infrastructure examples include Ethereum using ETH token for its decentralized stakers to help secure the Ethereum blockchain; Filecoin leveraging FIL token to coordinate its decentralized providers to supply file storage services; Chainlink using the LINK token to orchestrate a decentralized group of operators to provide off-chain data oracle services.

- Many Decentralized Finance (DeFi) protocols fall into the application product category. For example, AAVE is a lending and borrowing protocol. It has a safety module that rewards AAVE token holders for helping secure the platform in case of a deficit. In addition to the utility of participating in the safety module, AAVE token holders also hold full governance power to make decisions on the adjustment and improvement of the protocol. This type of governance structure is often used in Decentralized Autonomous Organizations (DAOs).

- Examples of human-oriented services include various types of DAOs. BitDAO is an investment DAO that owns billions of assets. Its BIT Token holders vote to invest in builders of the decentralized economy. DeveloperDAO is a SocialDAO formed by a community of builders with the goal of onboarding developers and building tools for Web3. It started with an NFT-based one-person-one-vote system and migrated into a fungible $CODE token to differentiate the voting rights between different levels of contributors.

In summary, using the above three types as a starting point and mapping them into the project specifics can help us sort out what crypto can do and whether a native token is needed for the project.

Crypto for different economic sectors

Crypto products facilitate transactions that form crypto economies. Meanwhile, crypto economies are also the results of integrating crypto with our existing economic sectors, e.g., the real or financial economy, and the physical or virtual economy. Therefore, the other perspective of examining crypto-product fit is the relationship of crypto with these different economic sectors.

Crypto economies

The real economy involves producing and consuming actual goods and services (such as food, clothing, houses, and machinery). It is determined by the demand side (what people want about the goods and services) and the supply side (cost of producing those goods and services).

The financial economy deals with the transaction of money and other financial assets. These financial assets are often tied to real assets in one way or another. E.g., stock certificates represent claims to ownership of real economy sectors. Credits from the financial economy flow into the real economy to help grow its productivity.

Both the real economy and the financial economy can reside in the physical or virtual worlds. A prominent example of an economy in a virtual world is a massively multiplayer online games platform allowing virtual goods and services exchanges.

These different types of economies can be summarized in the table below:

Real vs. financial economy and physical vs. virtual world

Real vs. financial economy and physical vs. virtual world

Both the real economy and financial economy sectors, whether physical or virtual, may integrate with crypto. Crypto is a vital force propelling the fusion of these different types of economies. The result of this process is a hybrid economic form that blends real and financial assets both in the physical and virtual world, also known as Metaverse economy. While there have been many activities in the virtual financial economy sector, a lot more developments in the virtual real economy sector need to be made in order to advance the metaverse economy agenda.

Now, let us explore more details on crypto for the financial economy and the real economy, respectively.

Crypto for the financial economy

The earliest crypto projects emerged for the financial economy. E.g., Bitcoin, the first and foremost crypto project, tackles the financial payment system. There are a couple of major themes in the crypto and financial economy intersection:

- Creating a decentralized version of financial economies in the crypto world on top of blockchains. Numerous DeFi applications launched so far fall into this category. Examples include asset exchanges like Uniswap and Curve, and banking institutions for lending and borrowing such as AAVE and Compound. Various stablecoins, such as DAI, are also notable cases in this category.

- Connecting and integrating the new crypto-based financial economies with traditional ones. For example, Synthetix is a crypto platform that enables trading derivatives of real-world stocks and commodities in the crypto land. The MakerDAO DeFi protocol is offering a $100M commercial loan in DAI to a community bank in Philadelphia, Huntingdon Valley Bank, marking “the first commercial loan participation between a US Regulated Financial Institution and a decentralized digital currency.” BlockTower Credit partnered with MakerDAO and Centrifuge to bring $220M of real-world assets to DeFi.

Crypto for the real economy

Crypto’s connection with the real economy can appear less straightforward than with the financial economy. Part of the reason is that by its nature, the real economy deals with mainly physical, tangible parts of the world, and crypto, on the other hand, is digital at its core. But there could still be plenty of use cases at the intersection of crypto and real economy sectors. The speed of various industries’ onboarding into crypto is expected to differ substantially. We can get some clues from how the overall digital transformation process has manifested in different sectors. According to a Harvard Business Review study, the ICT (Information and Communications Technology) sector is the most digitalized industry overall, and the agriculture & hunting industry is the least digitalized. These results are not surprising because the ICT industry happens to be the one that digitalizes all other industry sectors. Meanwhile, agriculture & hunting relies heavily on non-digital work. Aligned with these observations, we expect to see more established real economy crypto projects appear first in the more digitalized sectors, especially the ICT industry.

Similar to crypto for the financial economy, we are seeing two important themes in crypto for real economy projects:

- Leveraging crypto-mechanism to create a peer-to-peer version of real-economy business models. For example, in the ICT sector, Filcoin and Arweave are building decentralized file storage service networks; Helium is creating peer-to-peer wireless communications networks.

- Integrating crypto mechanisms into existing real-economy businesses. For instance, Brave is a browser released in 2016, and it launched its BAT token in 2019 to support its Ads system.

Product-Market fit: sustainable value creation

Crypto-product fit is only a necessary but not sufficient condition for a crypto product’s success. The other key test is whether it can achieve product-market fit. A product-market fit requires a healthy and consistent balance between the product’s supply and demand, resulting in sustainable economic value creation.

One common signal of a lack of product-market fit can be derived from the product’s demand situation. Helium is a high-profile crypto project that received top VC support. The project is building a peer-to-peer wireless Internet-of-Things (IoT) network service using token-based incentives. Yet the weak demand for its network triggered a heated debate over whether it is a perfect crypto real economy use case that is faster and more capital-efficient than traditional telecom infrastructure, or whether its crypto-economics simply could not work. In 2022, the team partnered with T-Mobile to further provide 5G services, with a new token launch and continued search for product-market fit. Another high-profile real-economy use case is a collaboration between IBM and Maersk, which aims to create a blockchain-based trading platform to streamline the supply chain industry. Unfortunately, it was recently shut down due to a lack of industry buy-in.

Even if the crypto-product has a strong demand, its business model that serves the demand could still be unsustainable. A lesson we can draw from the crypto financial economy is the Terra UST stablecoin project. One of the most well-known crypto projects that received capital from numerous respected VCs in the industry, the project saw an overwhelming market demand by amassing a 30B market cap at its peak. Yet it still collapsed due to fundamental flaws in its business model.

Proving or evaluating whether a project achieves product-market fit is not an easy task. One way that can help shed light on this direction is by examining its financial data, e.g., through the fees, revenues, and earnings of the projects. Websites such as tokenterminal provide related information.

Note that it is not uncommon for crypto projects to experience negative earnings during their growth stage. Leading DeFi protocols such as Curve, Convex, dYdX, have all been operating with negative on-chain profits with their token emission incentives. But they also rank among top protocols that generate fees or revenues. So they are trying to acquire users by subsidizing them. We see similar strategies used in non-crypto technology startups all the time. Companies like Amazon and Tesla lose money during years of initial growth period before becoming profitable. Eventually, the fundamental soundness of the business model and/or whether the team can pivot appropriately will determine the project’s success in the long term.

Back to “Why Token?”

With a good understanding of crypto-product-market fit, we are ready to come back to the original question of why a project would need a token.

Recall that more precisely, the question is about “Why create NATIVE tokens” for that project? We actually addressed that question when we discussed the role of crypto in the three basic crypto-product business models in the earlier section, which we can summarize again below:

- Type A crypto products that focus on processing exogenous tokens do not need their own tokens for their core operation. However, they could opt to introduce a token for other purposes, as appropriate. For example, the Uniswap crypto exchange does not need a token to operate, but it introduced its UNI token for governance. This also makes it a hybrid Type A and Type C business model.

- Type B crypto products, by definition, require creating their native tokens. For example, if we are issuing a new fiat-backed stablecoin by tokenization of a fiat asset, the stablecoin is the required token because it is the product itself.

- For Type C crypto products, if its token serves a utility essential for the product, such as an incentive token that helps secure the infrastructure (e.g., ETH for Ethereum blockchain and BTC for Bitcoin blockchain), then it is required. If the token is used for other purposes such as governance, then the answer is “maybe” because many applications or human-oriented services may bootstrap without a token. But they can later launch the token when they are ready to decentralize. We will elaborate on this point in our subsequent “When token” discussions.

Conclusion

This article examines the “Why token?” question that token designers need to consider before launching a token. Addressing this question starts by studying the underlying business model associated with the potential token, particularly the “crypto-product-market fit”. We first explored crypto-product fit by looking at crypto’s roles in the products and how crypto integrates with different economic sectors. Then we discussed product-market fit which ensures sustainable economic value creation from the product. Finally, we summarized the rule of thumb on whether the common crypto-product business models need a token.

“Why token” is the first “W” in the “W5H” framework of thinking, we will explore the remaining “W” in the next article.

This article is part of the six-part W5H framework for token design series, as listed below:

Related Articles

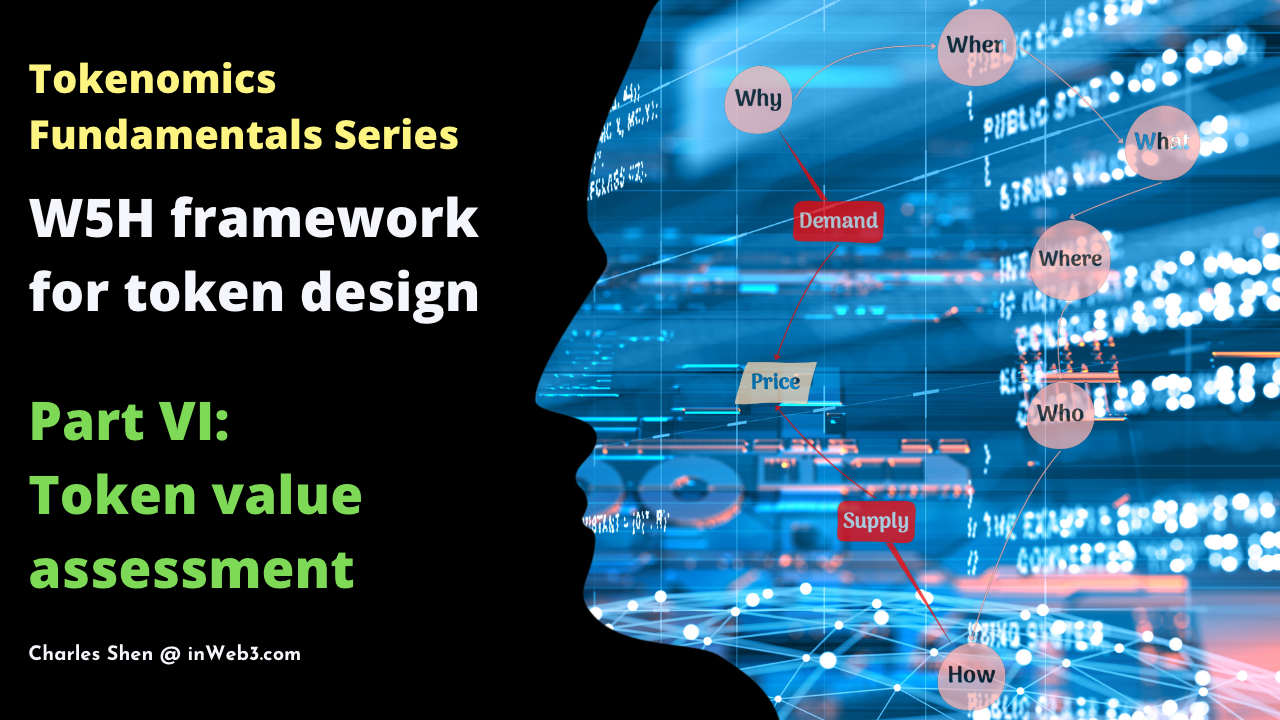

Tokenomics Fundamentals Series: W5H framework for token design, Part VI - Token value assessment

W5H tokenomics framework Part VI: token value assessment through TradFi modeling and their caveats, and a brief introduction to Token Engineering.

Tokenomics Fundamentals Series: W5H framework for token design, Part V - Token value accrual

W5H tokenomics framework Part V: token value accrual through universal and selective economic value distribution in crypto-economic systems

Tokenomics Fundamentals Series: W5H framework for token design, Part IV - Token supply and demand dynamics

W5H tokenomics framework Part IV: following "Why, When, What, Where, Who and How" for token design, we discuss token supply-demand dynamics